IRS Powers of Attorney: New FILING Options

Trusts & Estates, Tax Update

IRS Powers of Attorney: New FILING Options

A qualified tax professional may represent a taxpayer before the IRS. The tax professional is named in a power of attorney signed by the taxpayer.[i] The IRS power of attorney form is Form 2848 (“2848”).[ii]

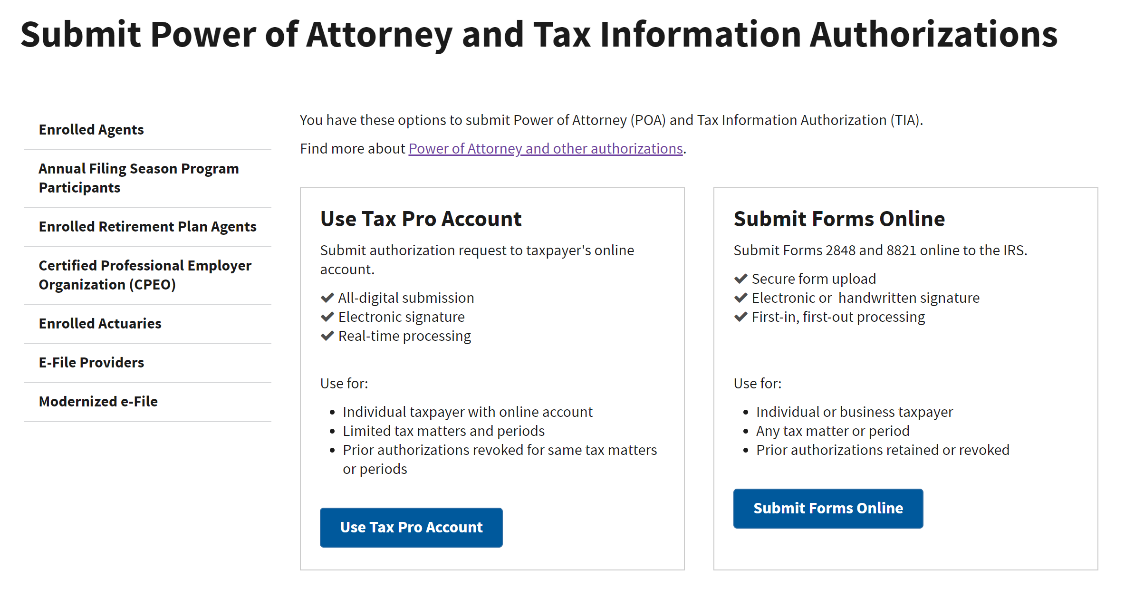

A. FILLING OPTIONS. There are now up to four ways to file a 2848. They are by mail, by fax, by online submission, and by using a Tax Pro Account. This link is to the IRS webpage where each of these methods can be accessed; a copy of that webpage is shown here:

1) The Traditional Method (Mail and Fax). A 2848 can be mailed or faxed to the IRS. The signatures must be handwritten (wet ink signatures). An electronically signed power of attorney cannot be mailed or faxed.

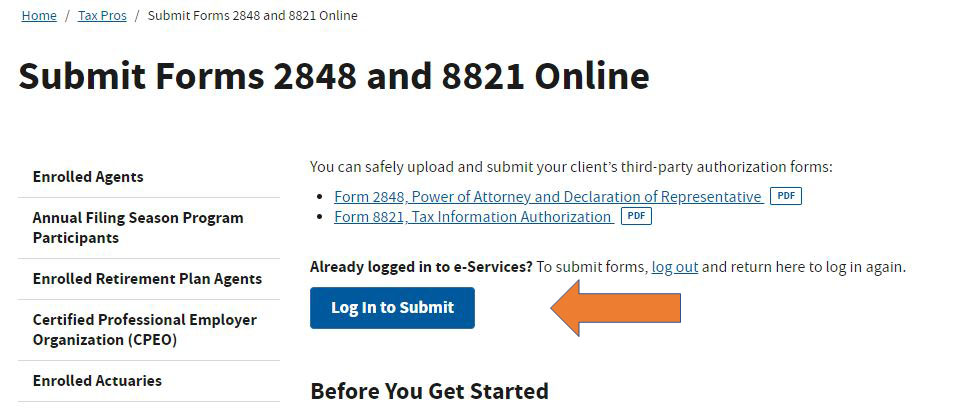

2) Upload Through IRS Website. If a 2848 is signed electronically, in whole or in part, a tax professional with Secure Access credentials can upload the 2848 on the IRS website. An online submission is processed along with 2848’s delivered by mail or by fax. The processing is not accelerated because the submission was made online.

- The IRS has explained that an “electronic signature” encompasses more than just a “digital signature”. No particular signature technology is required. The IRS has said an electronic signature includes a typed signature, a scanned or digitized image of a handwritten signature, a handwritten signature written onto an electronic signature pad, and a signature created using third-party software.

- A tax professional can create a Secure Access account at IRS.gov/Submit2848 by clicking the “Log In to Submit” button and following the instructions to “Create Account”. It is possible to complete the sign-up process in about 15 minutes, but it requires having a US-based mobile phone. Without a US-based mobile phone, the verification process is done by mail.

?

3) Use a Tax Pro Account. The IRS launched Tax Pro Account in July 2021. The IRS verifies the identity of both the tax professional and the taxpayer. The tax professional and the taxpayer each needs an IRS account.

- The tax professional enters the information needed for the authorization through the professional’s own Tax Pro Account. When that is finished, the IRS notifies the taxpayer. The taxpayer authorizing the representation then uses his or her own IRS account to complete the authorization. No 2848 is required. The authorization can be active immediately but should be active within two business days.

- Until further notice, Tax Pro Account cannot be used to authorize representation for an entity. Only an individual taxpayer may authorize a representative through Tax Pro Account.

- Not all individuals can give authorization through Tax Pro Account. An individual who cannot create and access an IRS online account is unable to authorize a representative through Tax Pro Account. An individual who does not have an address in the 50 United States or in the District of Columbia also cannot authorize a representative through Tax Pro Account.

- When a taxpayer logs in and opens his or her personal IRS account, the taxpayer will have various options on the home page of the account. This is what the tabs look like:[iii]

- By clicking on the Authorizations tab, the taxpayer can authorize a tax professional to represent him or her before the IRS.

B. UPLOAD VS. TAX PRO ACCOUNT. A primary difference between filing online and using the Tax Pro Account is the taxpayer identity verification process.

1) Tax Pro Account: IRS Verification. When using the Tax Pro Account, the IRS verifies the identity of the signing parties.

2) Uploading 2848: Uploader’s Verification. If the person who uploads a 2848 was not physically present when the taxpayer signed the 2848, the person uploading the 2848 must authenticate the taxpayer’s identity. Authentication is not required if the person already has personal knowledge of the taxpayer’s identity by reason of a business or personal relationship with the taxpayer.

3) Authentication. The person submitting a Form 2848 online authenticates the taxpayer’s identity by:

- Inspecting a valid government-issued photo id to compare it to the taxpayer. That comparison could be done by having the taxpayer send a self-taken picture of the taxpayer, by having met in person, or by having met by video conference.

- Recording the name, social security number, address, and date of birth of the taxpayer.

- Verifying the taxpayer’s name, address, and social security number through secondary documentation. This documentation could be, for example, a tax return, an IRS notice or letter, a social security card, a credit card, or a utility bill.

- If the taxpayer is an entity, confirming that the individual who is signing on behalf of the entity has authority to sign on the entity’s behalf.

C. IRS AWARENESS CAMPAIGN. The IRS has prepared handouts, which can be seen here and here.

[i] A taxpayer can also authorize a third party to inspect and receive confidential taxpayer information. IRS Form 8821 is used for this purpose. Form 8821 does not give a third party the right to represent the taxpayer or to speak on his or her behalf. The same procedures for filing a 2848 apply to a Form 8821.